Artificial Intelligence in Banking— Data-driven Business Models as the Future for Banking

Dr. Shivaji Dasgupta, Managing Director, Head of Data and Artificial Intelligence, Deutsche Bank

Henry Byers, Strategic Data Lead, Deutsche Bank

For banks, artificial intelligence is a key prerequisite to be sustainably successful in the future. What has been missing so far are standardized and innovation-friendly regulatory guidelines. This is where the government and the regulator are called to action.

Almost every industry is challenged by digitalization. While incumbents are under pressure, new technologies enable enhanced services and therefore stronger customer relationships.

Banks are no exceptions to this trend. On the contrary: Digital neo- and nonbanks are entering the market of traditional players even faster and establishing new business models. The trend in financial industries runs towards platforms as well as business models based on customer data. Banks which want to remain relevant and even more successful within this transformation process need to refocus their approach and therefore act like Amazon or Netflix. They have to use data as an enabler to recommend exactly those products to customers which are most suitable based on interests, user behavior, age or gender.

Resources of platforms are user data

Banks become platforms on which products and services will be offered that go far beyond the original banking business. Banks already have holistic data of their customers. By incorporating additional data and conformation of usage by the customer, his needs can be analyzed and tackled more comprehensively and thus better satisfied.

No use of artificial intelligence without a clear data strategy

Deutsche Bank derived the data strategy from overall ambitious targets. Digitalization is based on two cornerstones. On the one hand, the strategy is facing the transformation of the core business. On the other hand, attracting new markets and target groups is key. In this context the bank develops new products and services beyond banking and therefore collaborates with third party providers via an open data interface formally known as DB API.

Transforming the core focuses on data-driven redesign of products, for example when the customer opens an account or requests a loan. The current available customer profile provides important data for such transactions. This includes age and derived living conditions, his previous spending behavior, on what he clicked or processed in online or mobile banking or which offers he is interested in. This allows an individual, tailored product offering which is leading to increased customer satisfaction. When attracting new markets or target groups, real-time services, such as analyzing of contracts or spending behavior, bring an added value.

Artificial intelligence can support transforming the core as well as developing new digital business models, if it identifies current service gaps in existing products or from external data sources. Today “marketing and sales” is the most evident area. In this area demand and product related wishes of the customer can be forecasted and enhanced: For example, whether the customer is eligible for mortgage financing after starting his career and getting married, or whether he might be interested in investment products due to excess liquidity. Derived from this, customer touchpoints can be improved based on his current demand and process efficiencies for the bank as well as new revenue streams are enabled. Also, implementation of Artificial Intelligence will have a major impact for risk management. An advantage compared to traditional credit report, e.g. German “Schufa”, can be achieved when connecting external customer data with internal transaction data.

Connectable data architecture as basis

Use-Cases based on customer data need to be developed, tested and implemented accurately. Therefore, a sophisticated data strategy is required. It must be expandable based on the maturity level of respective use-cases. Diversity of data in artificial intelligence and use-case context needs opensource software and cloud technology.

Data architecture means the technical approach to store and use data: It starts with collecting data by linking and aggregating valuable data sources to a storage environment. Their statistical methods and models are used to ensure analytics and to make data technical visible. This means complex rows of numbers getting transformed into a presentable and easy to read format like charts. It is important to ensure multiple usability and aggregation of the data instead of just satisfying a single use-case.

Such data can be found in the transaction history of the customer within bank systems or in customer behavior data on external digital applications. This also can be based on publicly available data, like social media or even temperature and shutter settings in the apartment based on “smart home”.

Connectable data architecture as basis

Extensible data architecture does not automatically require Artificial Intelligence. Even more, Artificial intelligence should rather be used depending on a specific use-case. Depending on the complexity of the usecase it might make sense to rely on statistical methods for data analysis.

Germany needs a secure legal framework for artificial intelligence

In some European countries, such as the UK, there is the possibility of testing use cases based on artificial intelligence in laboratories (so-called sandboxes) within a legal secure framework. This would also be important for German countries. However, there is no legal framework for such an approach in place yet. The regulator is therefore asked to establish one. An example of a use cases to be testes is credit scoring. Currently, banks in Germany can only utilize scoring models that have been approved by regulators. This means banks have no opportunity of incorporating additional data to increase the evaluation and build products more suitable for the customer. As an example, smart home information could be used to assess the sustainability or thriftiness of the customer. This insight could have a positive impact on their creditworthiness. It could also be used to simulate the potential career opportunities of a current student with regard to the chosen courses in university. Based on this the bank is able to determine the risk of a credit more accurately. Such examples highlight the urgent need of “sandboxes” in order to test alternative assessment methods under real conditions.

Last but not least, additional data, for example when evaluating the creditworthiness, is leading to make it easier for people in our society to access banking services that were previously barred. Anyone who is experienced in obtaining a loan as a student at acceptable conditions if not being eligible for BAföG, will see the inclusion of external data from social media, university or “smart home” with different eyes. This can be transformed to the creditworthiness of refugees with the right of residence who wishes to establish a livelihood. The positive effect of using credit scoring based on artificial intelligence is that better and more accurate data enables the bank not to increase the risk of credits while expand lending at the same time.

Companies must prepare their employees for transformation of work

Artificial intelligence is already changing the profiles and skills of many areas in the banking business. It is foreseeable that this process will accelerate even further. For example, requirements for simple cognitive skills will tend to decline in the future, as these can be taken over by artificial intelligence. In contrast, the demand for technological as well as emotional skills will increase. New job profiles and new roles in the company are needed. Companies should prepare their employees for these change processes today and provide them with further training. In the future, for example, mathematicians have also be able to code. And classic database administrators should know what to do with cloud applications. Last but not least, project related work will increase while job profiles tailored to one specific area of work will decrease.

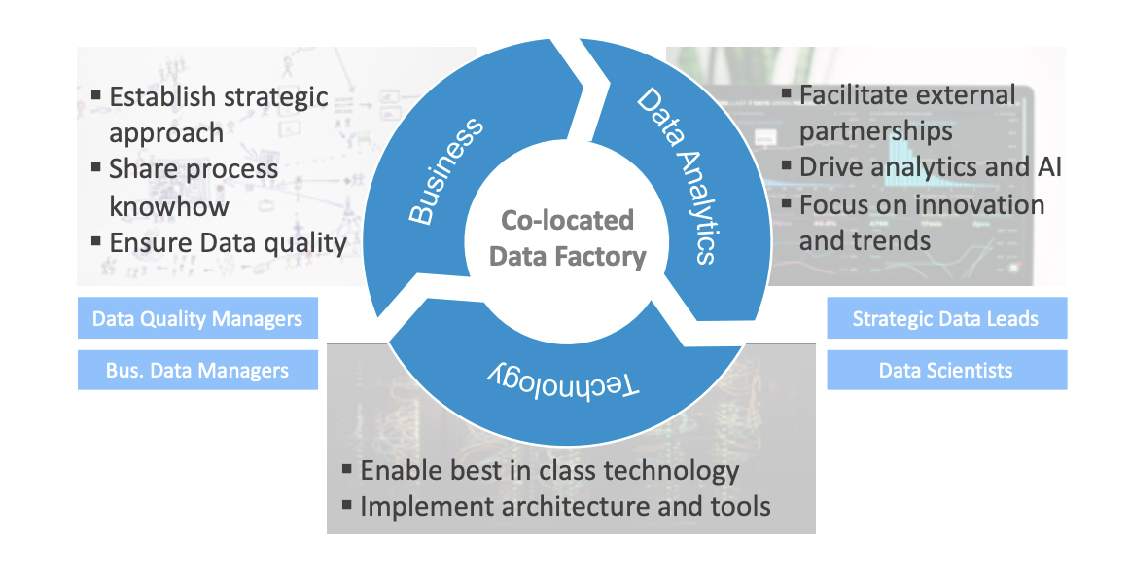

Data Factory ensures sustainable implementation of use cases and data-driven business models

To ensure the success of data-driven business models it will be necessary that business staff is working closely with their colleagues from IT and data analytics on an ongoing basis. Ideally, these people should be working in mixed teams, literally under one roof in so-called “co-located factories”: expert knowledge, technical expertise and statistical skills in banks need a common workplace.

Not everything that is technically possible is also socially desirable

Self-learning systems in the last instance of decision making always in human hands

Artificial intelligence has an incredible potential. However, ethical and cultural aspects as well as social responsibility must be taken into account. Democratic rights always mark the limits of what is doable when using artificial intelligence. This means that decisions are not allowed to the detriment of citizens. The final authority for self-learning systems must always remain the human being.